You can manage debt and protect your income with a careful strategy, enabling you to live comfortably without worrying about unforeseen financial setbacks. Here are some doable tactics to assist you in managing your tax exposure while repaying debts in your after-work phase.

-

Use Your Retirement Accounts Wisely

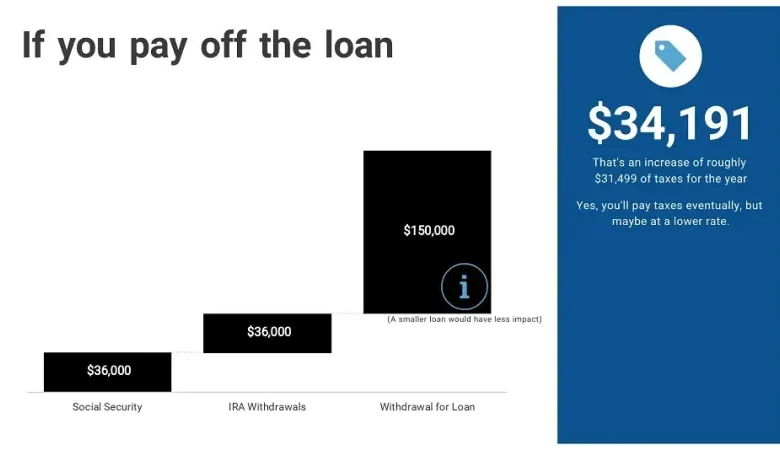

While tapping into these funds may seem like a quick fix, it’s important to consider the implications. By carefully timing your withdrawals, you can minimize the additional tax you may owe. This is a key aspect of executive retirement planning, where the goal is to ensure you can manage your financial needs without unexpected tax consequences.

-

Refinance or Consolidate Loans

You might be able to get a reduced interest rate through refinancing your loans, which would eventually lessen the overall cost. You can pay it off more quickly because you will be spending less on interest.

For example, Lamina offers loan refinancing services that could help retirees reduce their interest rates and consolidate multiple debts into a single, more manageable payment.

-

Consider Selling Assets

This can be a particularly useful option if you have significant equity in your home or other assets but want to avoid dipping into retirement accounts, which could result in a higher tax liability.

Don’t forget to take capital gains taxes into account when selling assets. Long-term capital gains rates are often better than regular income tax rates for assets kept for more than a year, which may lessen your liability.

Before selling, it’s a good idea to consult with a financial advisor, like a tax accountant in Ottawa, to better understand how the sale may impact your overall situation.

-

Take Advantage of Tax-Efficient Income Streams

Consider adding alternative income sources, such as dividends from taxable accounts, rental income, or annuities, to your income rather than depending too much on one source, like withdrawals from tax-deferred retirement accounts.

Since rental income is frequently taxed at a lower rate than ordinary income and because you can deduct related costs like mortgage interest, insurance, and property maintenance, rental properties in particular may provide tax benefits.

-

Pay Off Loans Gradually

You can avoid selling valuable assets or making significant withdrawals from your retirement savings by giving low-interest loans priority and making consistent, reasonable payments. By doing this, you can make sure that your revenue is steady and that you aren’t needlessly raising your tax liability.

The debt snowball strategy is one choice, in which you start by paying off modest loans and build momentum over time. The debt avalanche strategy is an additional technique that involves giving priority to loans with the highest interest rates.

You can continue to enjoy your retirement without feeling overburdened by your financial responsibilities thanks to both approaches’ realistic payment plans.

-

Minimize Your Living Expenses

Last but not least, cutting back on living expenses is a terrific method to get extra money that you may utilize to settle debts without affecting your tax status. Your cash flow can be greatly improved by reducing non-essential spending on things like luxury goods and eating out.

This is particularly crucial if you have a restricted retirement income and don’t want to take too many withdrawals from your accounts, which would raise your tax liability.

Retirement loan management doesn’t have to be a difficult task. You may pay off loans and maintain a modest tax burden by combining a number of wise tactics. You may enjoy your retirement without having to worry about debt if you take the time to plan ahead and get expert counsel.